Radio Advertising Forecast - 2021

25/02/2021 4:11 PM

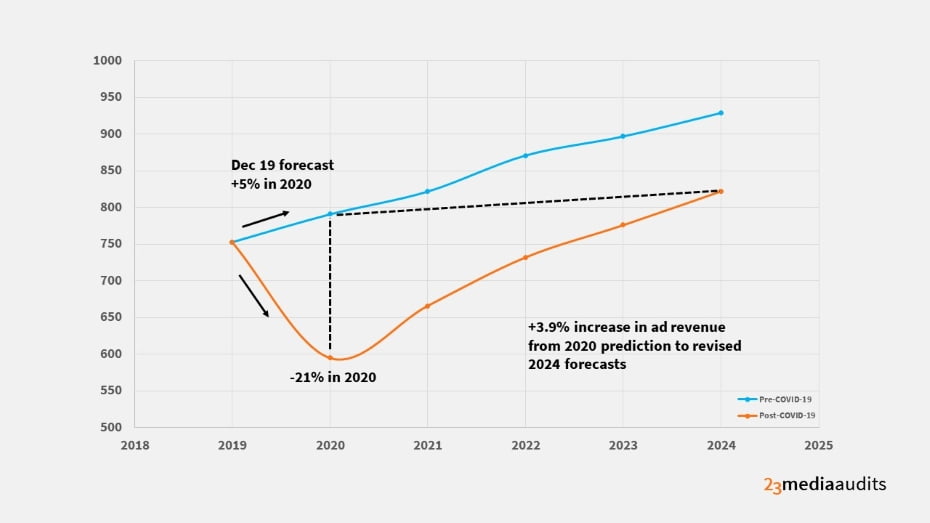

- 21% decline forecast for 2020

- 12% bounce back anticipated in 2021

- By 2024 radio will be ahead of pre COVID-19 predictions for 2020

- Evolving Ad models for 2021

- Global & Bauer to dominate commercial radio with prices to go up

A Year to Forget

Radio advertising in 2020 was predicted to see a 5% growth pre COVID-19 (+£38M on £753M). Unfortunately, the lethal cocktail of a global pandemic, national lockdowns, one of the worst recessions in history and mass retail closures has resulted in an unprecedented 21% decline in revenue and, in common with other media, this had had a profound effect on the industry.

A Gradual Recovery

However, striking a more positive note, with widespread vaccination and mass testing a priority in Q121 and the welcome opportunity of gradual relaxation of measures this brings, radio could potentially see a 12% revenue recovery in 2021 (up-to £666M). From this lower base we expect radio to then finally exceed its original pre-COVID 2020 forecasts by 2024.

Need some quick tips for your radio advertising? Download Our 10 Step Guide

Evolving Radio Ad Models

Radio, which is still reliant on spot advertising, has been working hard to push its digital offer which currently makes up an estimated 7.5% of spend and this is predicted to rise again in 2021.

Radio has seen some substantial advantage from audiences being at home more in 2020 and, aided by the use of smart speakers, this has helped partially offset any loss of audience resulting from less mobility via car travel and reduced on-site office/retail work. Interestingly, during the pandemic consumption of traditional radio is actually up in the UK due to shifts in consumer behaviour and the resulting change in how listeners consume audio.

However radio is also looking at other ad models to entice advertisers where the results are instant involving elements of service bookings and vouchers. Additionally we expect to see further growth this year in podcasting, which continues to deliver record numbers and currently has 14m average weekly listeners.

The Outlook for Radio Advertising in 2021

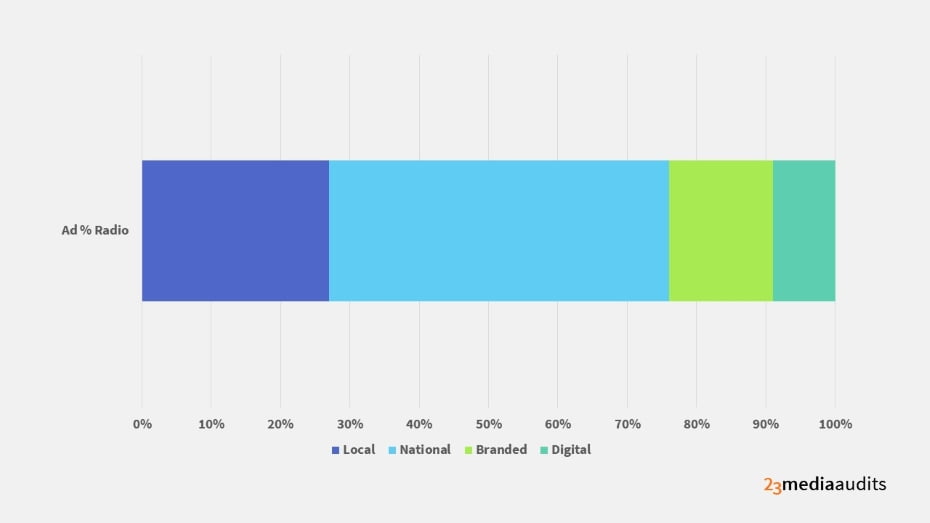

With 2020 RAJAR fieldwork on hold and pre-COVID-19 figures being used for agency trading we are expecting Heart and Global networks to be exceptionally busy in 2021, with opportunities for regionally targeted advertisers via Bauer and the series of stations that can deliver local targeting. It is absolutely vital that radio continues to looks after these local advertisers as they are predominantly made up of medium sized advertisers, challenger brands & regional advertisers who combined account for approximately a quarter of all advertising radio revenue.

We have already seen ad revenues impacted by the overall weaker advertiser demand and this was particularly apparent from local advertisers for radio. It is a cautionary tale and the potential risk in neglecting these brands is that they start to migrate to cheaper forms of digital advertising where the results can be quickly analysed across numerous metrics with the ability to stop or start at a moments notice.

We are also expecting to see the CPT rates becoming more expensive on radio as Global & Bauer dominate the buying opportunities available for advertisers. Inventory will potentially become restricted across the main networks of Heart & Capital, and with Bauer rebranding the local stations it acquired into its Hits Network the package deals for national advertisers will become the primary focus.

The Bottom Line

In summary we expect to see sustained audience benefit from on going ‘stay at home’ consumer behaviour that will continue to fuel audience demand. However the traditionally more expensive ad segments of breakfast and drive time may be affected by a reduction in the number of people travelling to and from work.

Although listener numbers may continue to rise, it will be a longer journey to see this trend reflected in actual revenue terms due to radio’s traditional reliance on local based advertisers. Demand is undoubtedly strong for podcasts and other digital audio formats; however, these make up only a small part of the radio revenue model and this ultimately limits their exposure to advertisers.

Radio obviously needs to keep exploring new revenue opportunities but there is a real danger of losing its lucrative local advertiser base to other digital platforms if it doesn’t work hard to protect this core base. Getting this delicate balance wrong could potentially hinder the growth levels expected for radio in 2021 and beyond.

We are also expecting to see the CPT rates becoming more expensive on radio as Global & Bauer dominate the buying opportunities available for advertisers. Inventory will potentially become restricted across the main networks of Heart & Capital, and with Bauer rebranding the local stations it acquired into its Hits Network the package deals for national advertisers will become the primary focus.

+12%

2.8%

7.5%

Our Radio Audit helps increase advertising effectiveness by saving you money.

To get started download our Radio Audit Guide which explains the process in more detail.