UK Adspend Showing Gradual Recovery in 2020 and into 2021

18/11/2020 4:03 PM

By Tony Emment

UK advertising spend is now forecast to recover better than expected for the full year. Looking back to the annual ad spend forecasts produced in April for 2020 we, alongside the industry, predicted the market to be down -16 to -20% year on year, however we are now expecting a decline of only -14 to -16%.

The Recovery

The above is a recovery of approximately £500M from initial April estimates with a strong Q3 leading the charge whilst Q4, although showing a gradual improvement, does not rebound to the level predicted back in April. One factor influencing this could be the UK’s own unique set of circumstances surrounding Brexit that will likely have an adverse impact on media activity. Current estimates also show that the UK is currently far weaker than both other European countries and the US in terms of GDP and for what ever reason this is stifling a quicker recovery. However on the plus side this could lead to a steeper growth curve in 2021 than we are currently forecasting.

The Advertising Association/WARC Expenditure Report has also recently amended its 2020 forecast to predict a decline of -14.5% in ad spend for this year. However, this is still based on the premise that we don’t have a continued lockdown and that there is a gradual return to marketplace normality.

To read more about this research click here to view the full article on Net Imperative.

Q4 2020

Back in April & July the forecast recovery was based upon the orderly scenario of businesses reopening and a subsequent solid economic recovery. There have been elements of this as Q320 improved more than initially expected and Q4 has improved again (especially in TV) but the overall market has not hit the levels expected back in April for Q4.

Q420 is proving difficult to judge in terms of revenue with the new lockdown now in place for November. There is a possibility that December could see delayed campaigns being moved into the final month. Although we saw a recovery after the first lockdown some traditional media providers are still struggling. We are still expecting to see a gradual improvement into 2021 and this will be led by digital and TV.

We still predict combined revenue from search, mobile, programmatic display and video to be down for Q420 at -4%, keeping the overall spend figures at a negative level and contributing to the total Q4 media spend down -11%.

Radio, OOH and Cinema, which together account for 12.0% of the total advertising market, are predicted to suffer further decreases (-31% collectively).

Finally, we are expecting an additional drop in the print market of -24% across Magazines, National and Regional print combined (including their digital revenues).

Overall, we expect the total 2020 market to be down between 14-16%.

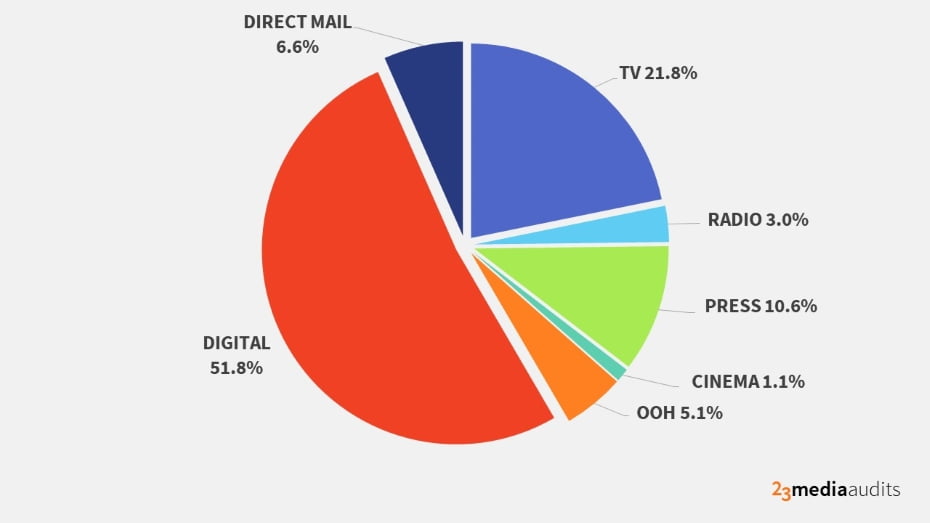

Q420 Media Share of Voice (Ad Revenue £) Predicted

Press comprises of national, regional newspapers & magazines. All above the line media includes their own digital revenues.

Q420 Media % YOY (Ad Revenue £) Predicted

2021 and Beyond

We still believe (as we mentioned back in Q2 when we reported on the current WARC forecasts for next year) that 2021 will not replace the major losses of 2020 and it will actually take all of 2021 and part of 2022 to do so. Leading us to comment at the time:

We don’t expect any increase until a vaccine is rolled out nationally and we see the benefit of large % increases in 2021. We believe the current WARC forecasts for next year will not replace the major losses of 2020 and it will actually take all of 2021 and part of 2022 as well to do.

So for many advertisers and the majority of media providers, 2020 will be a year to learn, move on from and prepare for the future with our expectation of a continued gradual recovery, gathering pace into 2021.

Our advice for 2021 would be to utilise all the knowledge gained from 2020 and use it to react quickly throughout the first half of 2021. Due to Covid19 your media agency may struggle to service all your planning and buying requirements and spend levels may have impacted your deal positions. Make sure for 2021 that you fully understand your media contract and safeguard the obligations in place. This is where the majority of our time is being spent to prepare for 2021.

Want better insights on how to plan your advertising campaigns during COVID-19?

Download our COVID-19 Advertising Report and bookmark our COVID-19 tracker for regular updates.